What do tulips, an 18th century import/export company, railways, Japan and technology all have in common?

Dec 20th, 2017The answer, of course, is that all have at some point been the subject of a speculative bubble.

Something might be considered to be in a bubble if its price far exceeds that which any reasonable fundamental analysis would otherwise arrive at.

Throughout history, assets and activities of all types have experienced this phenomenon, with the common theme generally being that the bubble has been all too obvious retrospectively, but significantly less so at the time.

Notable instances of asset bubbles in the past have been:

- Tulip Mania (1634-1637)

- South Sea Company (1720)

- Railway Mania (1840s)

- Japanese property and stock market bubble (1986-1991)

- Dot-com bubble (1995-2000)

All of these bubbles have demonstrated very similar characteristics, ultimately resulting in a collapse in value.

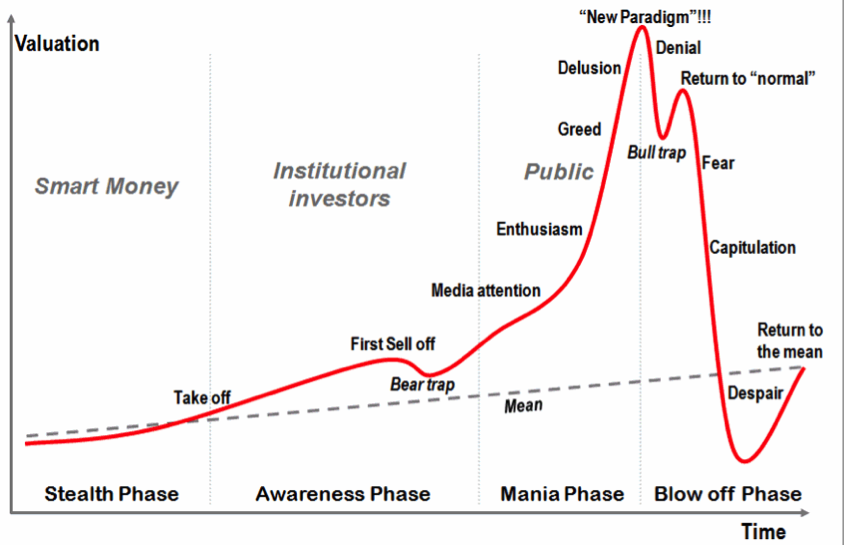

The Canadian scholar, Jean-Paul Rodrigue, neatly illustrated the four distinct phases of a bubble, in his model of economic bubbles (2008), shown in Figure 1 below:

Figure 1

It will no doubt not have escaped the reader’s attention that cryptocurrencies, in particular ‘Bitcoin’, have been featuring in the media recently, with growing regularity.

Stories are abound of those who have invested relatively modest amounts into this groundbreaking new form of currency, and are already well on their way to becoming digital millionaires.

It is well beyond the scope of this short blog post to attempt to begin to explain in detail how cryptocurrencies work.

However, the following, taken from www.coindesk.com, provides a succinct and easy to understand description of Bitcoin, a type of cryptocurrency:

Bitcoin is a form of digital currency, created and held electronically. No one controls it. Bitcoins aren’t printed, like dollars or euros – they’re produced by people, and increasingly businesses, running computers all around the world, using software that solves mathematical problems.

Whilst some might argue that a currency free from the control of a central bank (e.g. the US dollar or Sterling) is a truly wonderful thing and represents the first steps towards how all goods and services will be paid for in the future, there are others who see cryptocurrencies as an instrument with no intrinsic value and a bubble waiting to be burst.

The latter view is understandable when looking at how, for example, Bitcoin’s value relative to the US dollar has surged in 2017, as Figure 2 shows:

Figure 2

The cost to buy one Bitcoin has grown from $13.37 on 15th December 2012, to $16,706 (it is worth repeating this figure in words, sixteen thousand seven hundred and six dollars, for the avoidance of ambiguity) on 14th December 2017, an eye-watering increase of 124,851%.

From an investment valuation viewpoint, it would reasonable to take the view that Bitcoin is, in effect, worthless.

Whether ones believes in the fundamentals and principles of cryptocurrencies as a medium of exchange or not, it is difficult to look at the above chart and fail to draw comparisons with every other asset bubble in history.

Ardent supporters of cryptocurrencies will insist that this is an asset that deserves to be treated like no other, that it represents a fundamental change to the way things are done currently, and that it should not be valued in the same way that other types of asset (even other currencies) are currently valued.

Personally, I would argue that such a view is entirely consistent with the delusion and/or denial stages illustrated within Figure 1, and I invite the reader to draw their own conclusion as to where we presently stand in this regard.

It is worth stressing that out of the dot-com bubble in the late 1990’s came companies like Google, Amazon and eBay, corporate behemoths of the present day.

Likewise, the railway industry in the UK did not simply die out as a result of the collapse that followed Railway Mania in the 1840s.In fact, it laid the foundation for the modern day rail network.

Similarly, if (when) the cryptocurrency bubble does eventually explode, it should not be unexpected that the fall out will yield a surviving digital currency, or currencies, that will eventually form the foundation of a future global payment and transaction network.

However, an investment proposition with solid, measurable and reliable valuation fundamentals, cryptocurrencies are not.