Vanishing economic growth – Part 2

Sep 20th, 2022I have previously taken a sideways look at what is often referred to as ‘anaemic’ growth, and the origins of ‘sick man’ accolades in relation to a European nation. I was therefore quite pleased to see the following comment in Le Point International, a French newspaper, on 8th June, the day after the Conservative Party leadership contest.

“Boris Johnson est sorti très affaibli de sa victoire plus serrée que prévu lors de l'échec de la motion de censure déposée lundi par les rebelles conservateurs. S'il a sauvé son poste, le Premier ministre est confronté à une situation économique à ce point sérieuse que le Royaume-Uni est à nouveau considéré comme « l'homme malade de l'Europe ».”

So, perhaps unsurprisingly, at least one of our neighbours views us as the ‘sick man of Europe’.

Meanwhile, the OECD Economic Outlook published in June says the following about the UK economy, which it predicts will be 0% in 2023:

“GDP is projected to increase by 3.6% in 2022, before stagnating in 2023. Inflation will keep rising and peak at over 10% at the end of 2022 due to continuing labour and supply shortages and high energy prices, before gradually declining to 4.7% by the end of 2023. Private consumption is expected to slow as rising prices erode households’ income. Public investment will weaken in 2022 as supply bottlenecks hamper the implementation of planned investment, but is set to rise again in 2023 as these effects subside. A tight labour market will help to keep unemployment low.”

War in Ukraine has had, and will continue to have, significant negative impacts on millions of people, and the associated economic shocks will have a material adverse impact on economic outcomes and individual livelihoods.

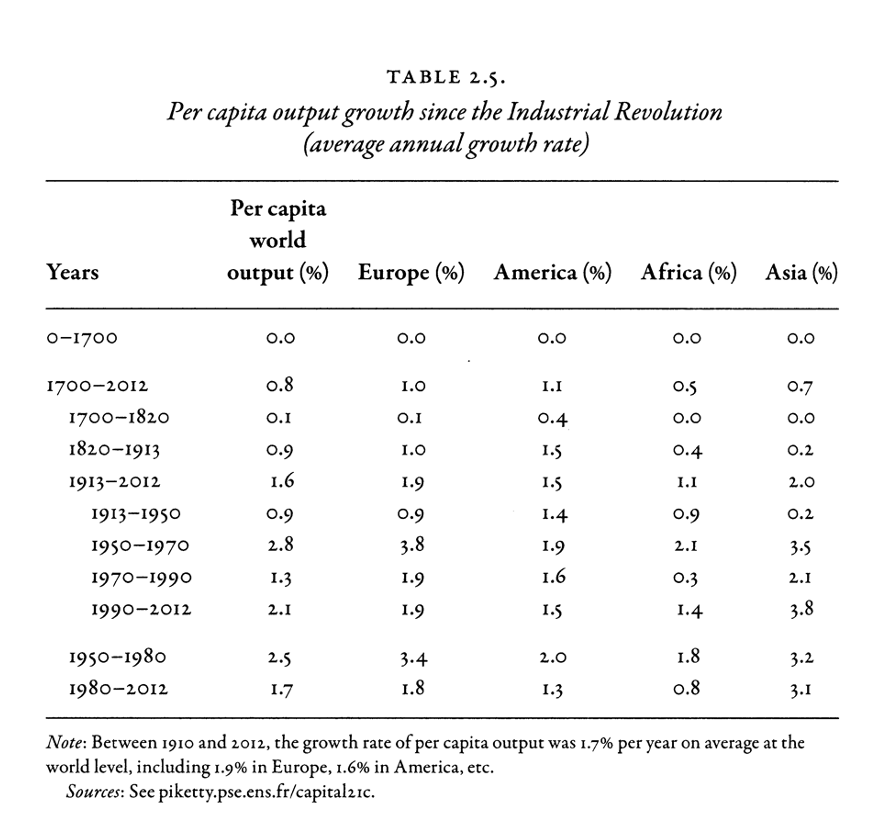

Stepping back from the here and now though, Table 2.5 is taken from Thomas Piketty’s Capital in the Twenty-First Century. In his view, the most important point – far more so than any specific growth rate prediction is his conclusion from the data that an annual growth rate of just 1% is in fact extremely rapid.

Piketty states that a society which grows at this rate, as the most advanced economies have done since the turn of the nineteenth century, is one that undergoes deep and permanent changes. After all, such a rate would lead to a doubling in per capita output during a single generation.

A society which grows at 0.1%-0.2% per annum clearly reproduces itself with little or no change from one generation to the next.

Growth rates of 3-4% per annum, which frequently fall from the lips of politicians, and often become normalised as reasonable expectations, have only ever occurred in countries that were experiencing accelerated catch-up with other countries. This process must end when the catch-up has been achieved, and such rates can only be transitional and temporary.

To state the obvious, the historic data reflects unconstrained burning of fossil fuels. Piketty concludes that a plausible (but uncertain) long run rate of growth in the wealthy countries would be 1.2% per annum, but that this level could not be achieved unless new sources of energy are developed to replace fossil fuels.

History therefore suggests that, far from being a sign of ‘anaemia’, low rates of growth are in fact to be expected.